Getting your first credit card in the United States feels like a classic catch-22. You need credit to get credit. Lenders want to see a history of responsible borrowing before they'll approve you — but if nobody approves you, how do you build that history in the first place?

The good news is that this problem has real solutions. There are credit cards specifically designed for people with no credit history, thin files, or a limited track record, and using one the right way can have you building a solid credit score within six to twelve months.

Here's what you need to know before you apply.

Why Building Credit Matters in the US

In the United States, your credit score affects more than just credit cards and loans. Landlords check it before renting to you. Some employers run credit checks as part of hiring. Utility companies may require deposits if your score is low. Car insurance premiums in many states are partly based on credit. And when you eventually want a mortgage, your score will directly determine your interest rate — which over a 30-year loan can mean tens of thousands of dollars difference.

Starting early and building credit responsibly is one of the most financially useful things you can do in your twenties, even if you never plan to carry debt.

Types of Starter Credit Cards

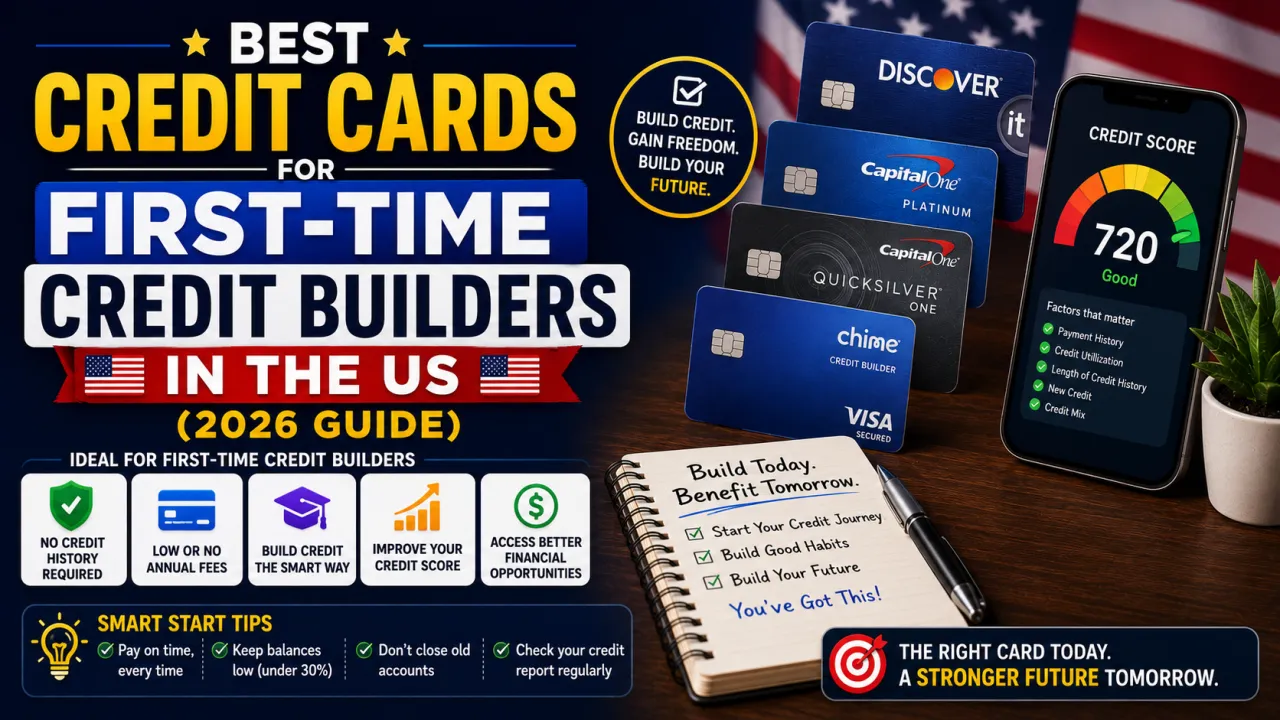

Secured Credit Cards A secured card requires a refundable security deposit — typically $200 to $500 — which becomes your credit limit. The card works exactly like a regular credit card for purchases, but your deposit protects the lender if you don't pay. Most secured cards report to all three major credit bureaus (Experian, Equifax, TransUnion), which is how you build your credit history.

After six to twelve months of responsible use, many secured card issuers will upgrade you to an unsecured card and return your deposit. These are the most reliable way to start building credit from zero.

Student Credit Cards If you're currently enrolled in college or university, student credit cards are unsecured (no deposit required) and are designed for people with limited or no credit history. They typically have lower credit limits and modest rewards, but they're a solid starting point.

Store Credit Cards Retail store cards are often easier to get approved for than general-purpose cards. They typically have high interest rates and can only be used at specific retailers, but they do report to credit bureaus. Use one only if you genuinely shop at that retailer regularly — and always pay in full.

Credit Builder Loans Not a credit card, but worth mentioning. Some banks and credit unions offer credit builder loans where you make monthly payments into a savings account and receive the money at the end. These report to credit bureaus and are an alternative way to establish history alongside or instead of a card.

What to Look for in a First Credit Card

Bureau reporting: Make sure the card reports to all three major credit bureaus — Experian, Equifax, and TransUnion. Some prepaid cards do not report at all and will not help build your credit.

Fees: Avoid cards with high annual fees, monthly fees, or activation fees. A starter card should cost you nothing or very little to hold if you're paying your balance in full each month.

Upgrade path: The best secured cards have a clear path to becoming unsecured. Look for issuers who will review your account after six to twelve months and either upgrade you automatically or allow you to apply to convert.

Interest rate: A high APR matters less if you pay your balance in full every month — and for credit building, you should. But it's still worth checking. A card with a 29.99% APR isn't a problem if you never carry a balance, but a single missed payment could be expensive.

Credit limit increases: Some cards offer automatic credit limit increases after a period of on-time payments, which helps your credit utilisation ratio.

Which Issuers Are Known for Starter Cards?

Rather than recommending specific products whose terms change frequently, here are the types of issuers consistently known for strong starter card options:

Major banks with secured card programs — Discover, Capital One, and Bank of America have historically offered secured cards with clear upgrade paths and no or low annual fees. Discover's secured card in particular has been consistently recommended by personal finance experts for its cashback rewards and automatic review process.

Credit unions — Local and national credit unions often offer secured cards with lower fees and more flexible approval criteria than major banks. If you have access to a credit union through your employer, school, or community, it's worth checking their card options.

Online banks and fintech lenders — Companies like Chime and Current offer credit builder products that work differently from traditional secured cards but serve a similar purpose. These typically involve spending from a secured account and having those transactions reported as credit.

Always compare current offers at sites like NerdWallet, Credit Karma, or Bankrate before applying — rates, fees, and approval criteria change frequently.

How to Use a Starter Card to Build Credit Fast

Getting the card is only step one. How you use it determines how quickly your score improves.

Keep utilisation below 30% — credit utilisation is the percentage of your available credit you're using. If your limit is $500, try not to carry a balance above $150 at any time. Ideally, keep it below 10% for the best score impact. This is the single biggest lever you control outside of payment history.

Pay on time, every time — payment history makes up 35% of your FICO score. One missed payment can set you back significantly. Set up autopay for at least the minimum payment as a safety net, then pay the full balance manually on your due date.

Pay the full balance monthly — carrying a balance costs you interest and doesn't help your credit score more than paying in full does. The score doesn't know or care whether you carry a balance — it just reports your utilisation at a given moment.

Don't close the account — length of credit history matters. Even after upgrading to a better card, keep your first card open if there's no annual fee. Just use it occasionally to keep it active.

Limit new applications — each credit card application generates a hard inquiry on your credit report, which can temporarily lower your score by a few points. Don't apply for multiple cards at once. Build history with one card for six to twelve months first.

How Long Does It Take to Build Credit?

With a secured or starter card used responsibly, most people see a measurable FICO score within three to six months. Getting from no credit to a "good" score (670+) typically takes twelve to twenty-four months of consistent, on-time payments and low utilisation.

Going from good to excellent (750+) takes longer — usually three to five years of clean credit history — but the biggest quality-of-life improvements in terms of loan approvals and interest rates happen once you cross 670.

Common Mistakes to Avoid

Applying for too many cards at once — lenders see multiple applications in a short window as a red flag. Space applications at least six months apart.

Maxing out your credit limit — even if you pay it off every month, a high utilisation at the time of reporting hurts your score. Keep balances low before the statement closing date, not just before the due date.

Ignoring your credit report — check your report at annualcreditreport.com (the official free source) regularly for errors. Incorrect negative marks can drag your score down and you have the right to dispute them.

Closing old accounts — closing a card reduces your total available credit and shortens your average account age. Both hurt your score.

The Bottom Line

Building credit in the US from scratch takes patience, but it's a straightforward process when you use the right tools. A secured card or student card, used for small regular purchases and paid in full every month, will build a solid credit history within a year. The key is consistency — there's no shortcut, but there's also no mystery. Show up every month, pay on time, keep your balances low, and your score will follow.

The Editorial Team

We are a collective of tech enthusiasts and digital experts dedicated to making sense of the evolving digital landscape for our global audience.

Connect With Us

0 Perspectives