If your credit history has taken some hits — or you've been denied a bank account due to a negative ChexSystems report — traditional banks can feel like they've closed the door on you. The good news is that a new generation of app-based banks has opened a different door entirely.

Chime, Current, and Dave are three of the most widely used neobanks in the United States, and all three are accessible to people with bad credit or no prior banking history. But they're different products, and choosing the right one depends on what you actually need.

Here's a real comparison.

What Is a Neobank and Is It Safe?

A neobank is a digital-only bank that operates through a mobile app rather than physical branches. They typically partner with FDIC-insured banks to hold your deposits, which means your money is protected up to $250,000 per depositor — the same coverage as a traditional bank.

None of Chime, Current, or Dave are banks themselves in the traditional sense, but all three partner with FDIC-insured banking institutions. Your money is safe. What you're comparing is the product experience, features, and fees — not safety.

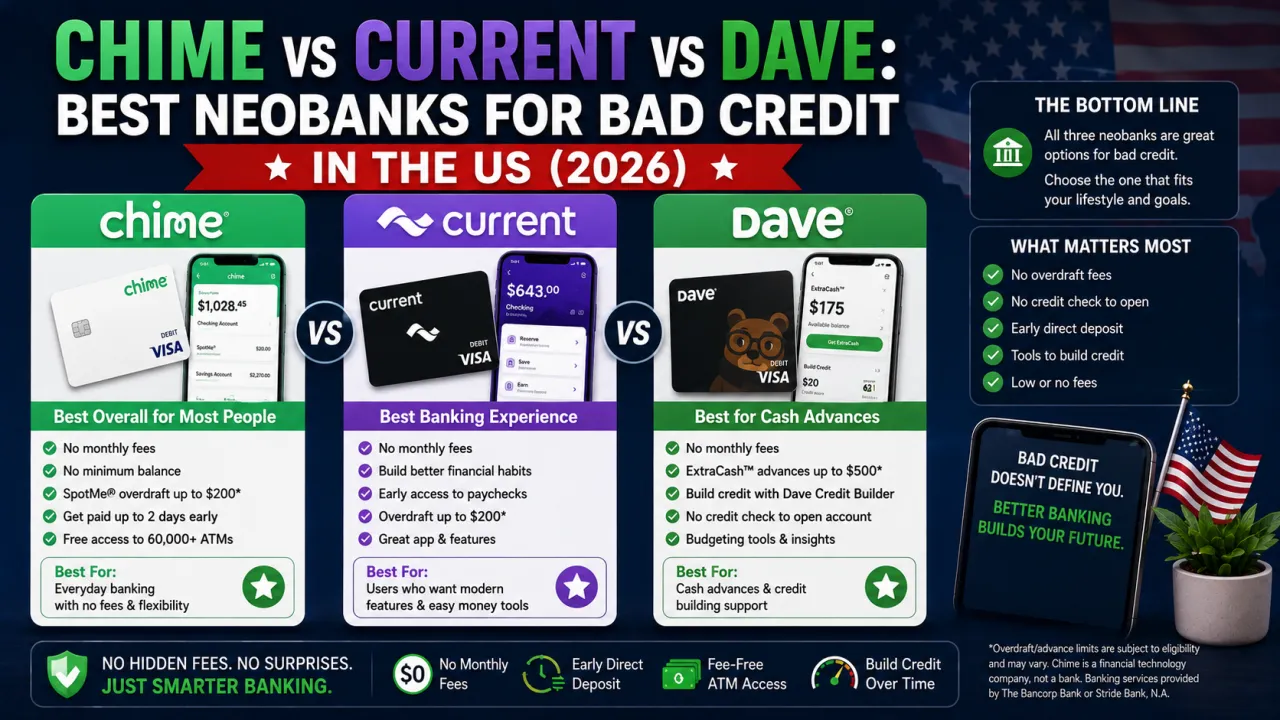

Chime

Chime is the largest US neobank by customer count, with tens of millions of users. It's built around simplicity and accessibility.

Key features:

- No monthly fees, no minimum balance

- No credit check to open an account

- SpotMe — fee-free overdraft coverage up to $200 for eligible members (based on deposit history)

- Early direct deposit — get paid up to two days early when you set up direct deposit

- Credit Builder — a secured credit card that reports to all three bureaus, helping you build credit with no hard inquiry required

- Savings account with round-up feature and automatic savings tools

- 60,000+ fee-free ATMs in the Allpoint and MoneyPass networks

What Chime is best for: People who want a straightforward checking and savings account with no fees, overdraft protection, and a clear path to building credit. The Credit Builder card is a genuine standout — it works by moving money you've already deposited into a secured account that backs your card spending, so there's no risk of debt and no interest.

Limitations: No joint accounts. Customer support is app and chat based — no phone number for general inquiries. Limited cash deposit options (you'll pay a fee at most retailers).

Current

Current is a New York-based neobank that's gained traction particularly with younger users and gig workers. It offers a fuller feature set than Chime in some areas.

Key features:

- No monthly fees on the basic account (Premium tier at around $5/month)

- No credit check to open

- Overdraft protection up to $200 with Overdrive (for qualifying members)

- Early direct deposit — up to two days early

- Points rewards on purchases at participating retailers

- Teen banking — a feature specifically for families wanting to give teenagers a supervised account

- Savings pods — separate savings pots within the app for goal-based saving

- Gas station holds — Current handles the temporary gas station pre-authorisation more gracefully than most banks, releasing the hold faster

What Current is best for: People who want slightly more features than Chime offers — particularly the points rewards system, teen banking, or the savings pods. Gig workers who receive irregular deposits also tend to find Current's deposit handling smooth.

Limitations: The points rewards system requires some engagement to get value from. Premium tier costs money. Cash deposits can be done at Green Dot locations but fees apply.

Dave

Dave started as an overdraft protection app and has expanded into a full neobank. It has a slightly different philosophy from the other two — more focused on cash advances and helping people avoid fees from traditional banks.

Key features:

- ExtraCash — cash advances up to $500 with no interest and no hard credit check (repaid on your next payday)

- No minimum balance requirement

- No overdraft fees

- Side Hustle feature — Dave connects users with gig work opportunities through the app

- Goal-based budgeting tools built into the app

- FDIC-insured through its banking partner

Monthly fee: Dave charges a $1/month membership fee — small, but worth noting since Chime and Current's basic tiers are free.

What Dave is best for: People who frequently find themselves a little short between paychecks. The ExtraCash advance up to $500 is the most flexible of the three for short-term gaps — no interest, no credit check, just a small optional tip. If you're in a pattern of living close to your paycheck, Dave gives you a genuine buffer.

Limitations: The $1 monthly fee, while small, is a difference. The ExtraCash advance has to be repaid when your next paycheck arrives, so it's a bridge, not a solution to larger financial issues. The feature set outside of cash advances is less developed than Chime or Current.

Side-by-Side Comparison

| Feature | Chime | Current | Dave |

|---|---|---|---|

| Monthly fee | None | None (basic) | $1/month |

| Overdraft protection | Up to $200 | Up to $200 | Up to $500 (ExtraCash) |

| Early direct deposit | Yes (2 days) | Yes (2 days) | Yes |

| Credit building tool | Yes (Credit Builder) | No | No |

| Rewards | No | Yes (points) | No |

| Teen accounts | No | Yes | No |

| Cash deposits | Limited | Limited | Limited |

| FDIC insured | Yes (via partner) | Yes (via partner) | Yes (via partner) |

What About ChexSystems?

ChexSystems is a reporting agency that traditional banks use to screen new customers. If you've had a bank account closed for unpaid fees or overdrafts, that record stays in ChexSystems for up to five years and can prevent you from opening an account at most traditional banks.

All three — Chime, Current, and Dave — do not use ChexSystems for account approval. This makes them genuinely accessible if you've been turned down by traditional banks.

Which One Should You Choose?

Choose Chime if you want the cleanest, most established neobank experience with the best credit building tool. The Credit Builder card is a real differentiator for anyone working on their credit score alongside their banking.

Choose Current if you want more features on top of the basics — particularly rewards, teen banking, or more sophisticated savings tools.

Choose Dave if you regularly find yourself short between paychecks and want access to a meaningful cash advance (up to $500) without credit checks or interest.

Can you use more than one? Yes, and some people do — Chime for day-to-day banking and credit building, Dave for the occasional short-term advance. There are no fees for having multiple accounts.

The Bottom Line

Bad credit or no banking history shouldn't leave you without options. Chime, Current, and Dave all offer real banking functionality, FDIC protection, and no hard credit checks to open. The right choice depends on what you need most — credit building, cash advances, or a fuller feature set. Any of the three is a significant upgrade over paying fees at a traditional bank or going without an account entirely.

The Editorial Team

We are a collective of tech enthusiasts and digital experts dedicated to making sense of the evolving digital landscape for our global audience.

Connect With Us

0 Perspectives